Utility Functions

EzTao also provides a series of tools to help you model and understand time series data using CARMA. They are in two categories: visualization tools and functions to compute 2nd order statistics.

Visualization tools (eztao.viz.mpl_viz)

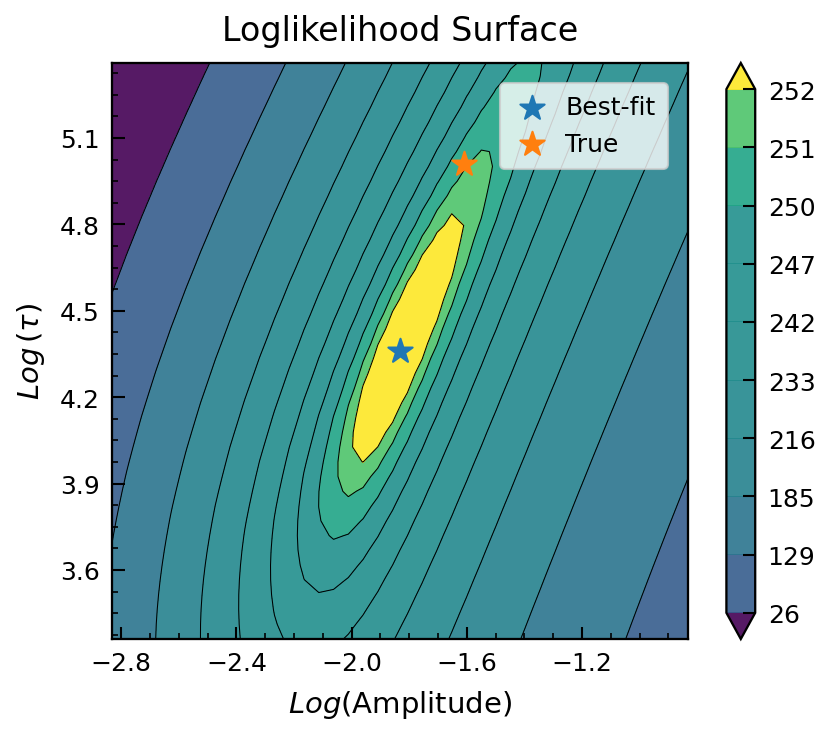

plot_pred_lc: Plotting the predicted time series given best-fit parameters conditioned on the input time series.plot_drw_ll: Plotting the log likelihood landscape of a DRW model.plot_dho_ll: Plotting the log likelihood landscape of a DHO/CARMA(2,0) model

[1]:

import numpy as np

from eztao.carma import DRW_term

from eztao.ts import gpSimRand

from eztao.ts import drw_fit

from eztao.viz import plot_pred_lc, plot_drw_ll

[2]:

# initialize a DRW kernel

amp = 0.2

tau = 150

DRW_kernel = DRW_term(np.log(amp), np.log(tau))

# simulate a process using the above model

SNR = 10

duration = 365*10.0

npts = 200

t, y, yerr = gpSimRand(DRW_kernel, SNR, duration, npts, log_flux=False)

# fit

best_fit = drw_fit(t, y, yerr)

print(f'Best-fit DRW parameter: {best_fit}')

Best-fit DRW parameter: [ 0.16008592 78.28325798]

[3]:

## plot predicted time series

t_pred = np.linspace(0, 365*6, 2000)

# get best-fit in CARMA space

best_fit_kernel = DRW_term(*np.log(best_fit))

best_fit_arma = best_fit_kernel.get_carma_parameter()

plot_pred_lc(t, y, yerr, best_fit_arma, 1, t_pred)

[4]:

## plot log likelihood surface

from eztao.ts import neg_param_ll

from celerite import GP

gp = GP(DRW_kernel, mean=np.median(y))

plot_drw_ll(t, y, yerr, best_fit, gp, neg_param_ll, true_params=[amp, tau])

2nd Order Statistics (eztao.carma.model_utils)

Given a valid CARMA kernel, you can generate 2nd order statistics at a range of timescales/frequencies. In this section, we will use a DHO/CARMA(2,1) model for demonstration. For a reference of how those statistics can be useful for analyzing time series data, feel free to check out Moreno et al. 2019.

PSD: Power spectrum density

ACF: Auto-correlation function

SF: Structure function

[5]:

from eztao.carma import CARMA_term

from eztao.carma import carma_acf, carma_psd, carma_sf

Create the PSD, ACF and SF functions given some DHO parameters

[6]:

ar = np.array([0.04, 0.0027941])

ma = np.array([0.004672, 0.0257])

psd = carma_psd(ar, ma)

acf = carma_acf(ar, ma)

sf = carma_sf(ar, ma)

Define a range of time scales and frequencies

[7]:

t = np.logspace(-1, 2.5, 1000)

t = np.insert(t, 0, 0)

freq = np.logspace(-5, 2)

Next, let’s try to plot them

[8]:

import matplotlib.pyplot as plt

[9]:

fig, ax = plt.subplots(3, 1, figsize=(6, 6), dpi=150)

ax[0].plot(t, acf(t), label='Autocorrelation')

ax[0].set_xlabel('Time (day)', size=10, labelpad=5)

ax[0].legend()

ax[1].plot(t, sf(t), label='Structure Function')

ax[1].set_xlabel('Time (day)', size=10, labelpad=5)

ax[1].set_xscale('log')

ax[1].set_yscale('log')

ax[1].set_ylim((10e-3, 1))

ax[1].legend()

ax[2].plot(freq, psd(freq), label='Power Spectrum Density')

ax[2].set_xlabel(r'Frequency ($\mathrm{\frac{1}{day}}$)', size=10, labelpad=5)

ax[2].set_xscale('log')

ax[2].set_yscale('log')

ax[2].legend()

fig.subplots_adjust(hspace=0.55)